Selling a business is rarely as simple as finding a buyer and agreeing on a price.

This guide walks through the full business sale process, from the first decision to the final handover so you can move forward with clarity.

Many Australian businesses turning over $5M–$20M believe their value is obvious.

Revenue is strong.

Clients are loyal.

The owner works hard.

But buyers price differently.

Owners focus on effort.

Buyers focus on risk.

Owners focus on revenue growth.

Buyers focus on sustainable EBITDA.

If you want to increase the value of your business before selling, you must understand how buyers actually assess it.

Value is rarely created in the final negotiation.

It is engineered 12–36 months before going to market, starting well before most owners realise they should be preparing to sell.

Buyers pay for certainty, not history.

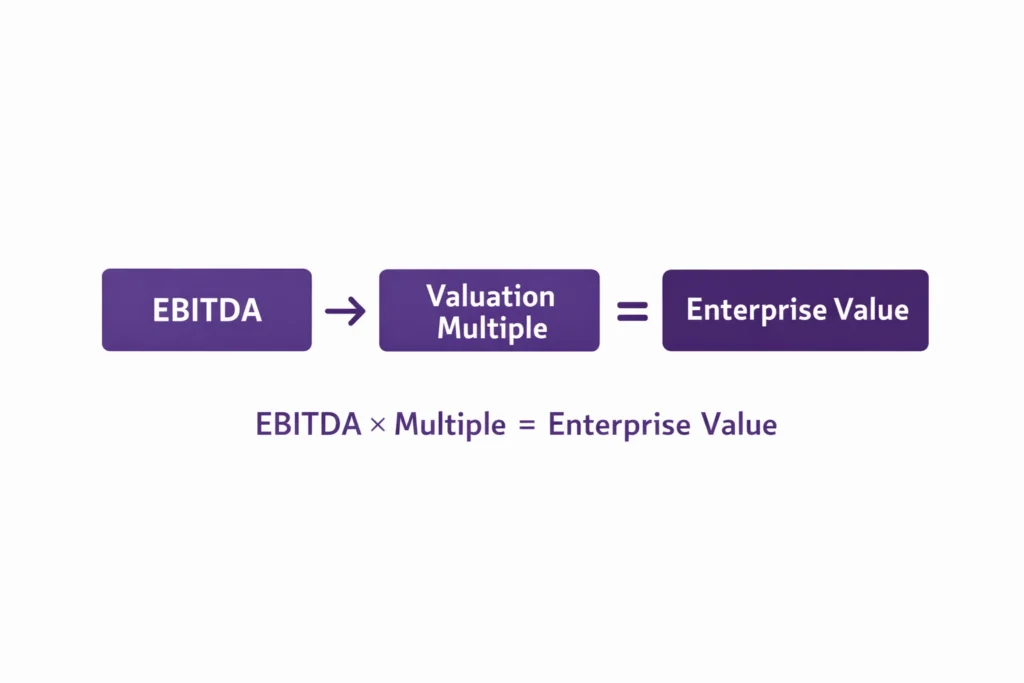

Most structured businesses in the $1M–$6M EBITDA range are valued using EBITDA.

EBITDA stands for Earnings Before Interest, Tax, Depreciation and Amortisation.

It measures the core operating profitability of the business independent of financing structure.

Enterprise value is typically calculated using:

EBITDA × Multiple

However, the multiple is not fixed.

It reflects:

• Risk

• Transferability

• Stability

• Scale

• Buyer demand

Example

Facilities maintenance business.

Revenue: $18M

EBITDA: $2.4M

Margin: 13%

If the multiple is 4.5x

Enterprise Value = $10.8M

If risk reduces and the multiple moves to 5.2x

Enterprise Value = $12.48M

Same EBITDA.

$1.68M difference.

The multiple often drives more value than EBITDA growth alone.

The multiple is a confidence score.

EBITDA scale influences who can buy your business.

At $1M EBITDA

• Buyer pool often consists of individual buyers or small operators

• Funding can be tighter

• Perceived fragility is higher

• Multiples may sit between 3.5x – 4.5x

At $2M–$3M EBITDA

• Broader trade buyer pool

• Some private equity interest

• Greater financing flexibility

• Multiples often move into 4.0x – 5.5x

At $4M–$6M EBITDA

• Institutional buyers appear

• Private equity becomes more active

• Competitive tension increases

• Multiples may reach 5.0x – 6.5x

Scale reduces perceived fragility.

Fragility influences pricing.

As EBITDA grows, buyer options expand.

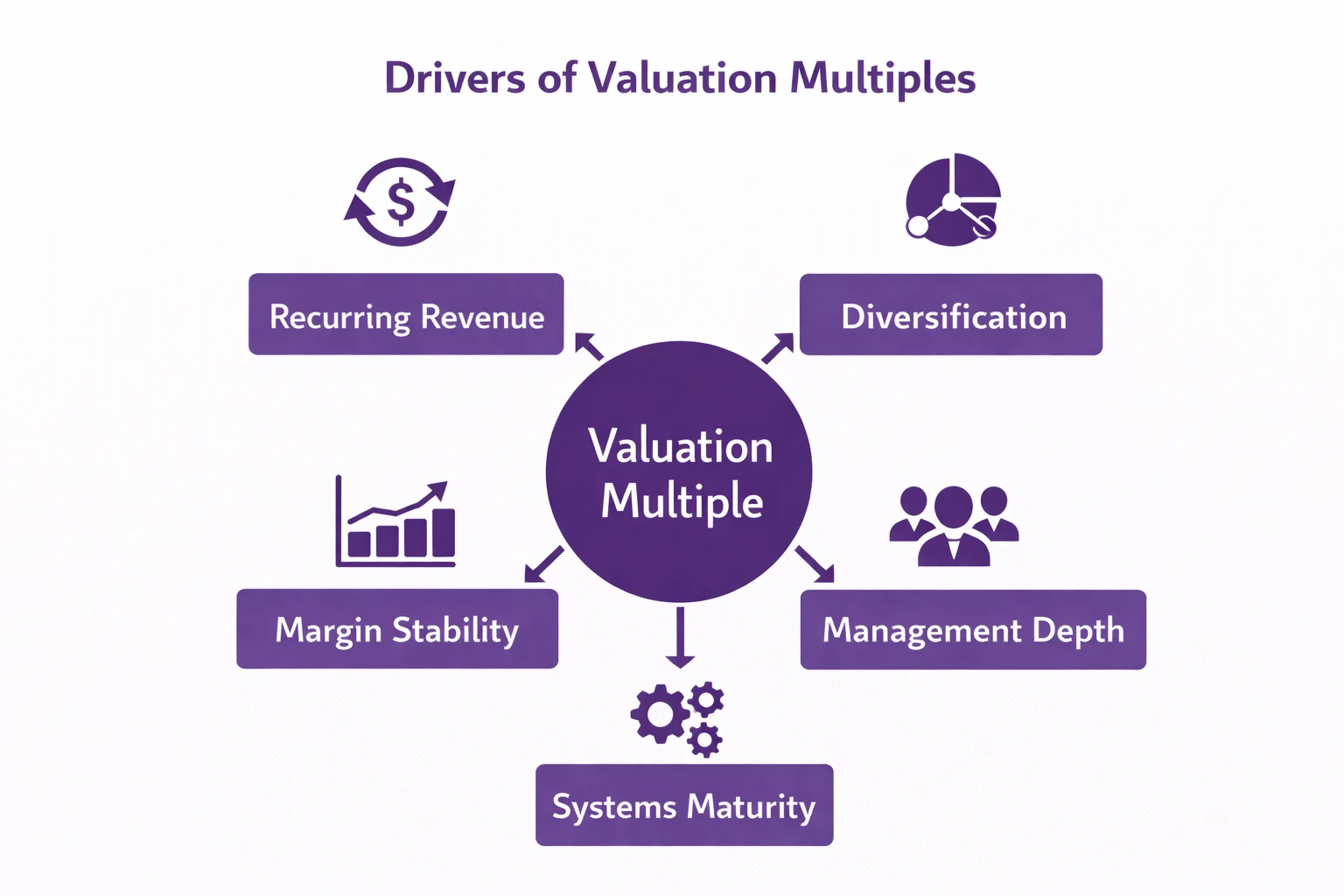

Multiples expand when risk compresses.

Key drivers include:

• Earnings consistency

• Revenue recurrence

• Margin stability

• Customer diversification

• Management depth

• Systems maturity

• Contract security

• Growth visibility

Each driver shifts perceived risk.

Risk drives valuation multiples.

If you want a deeper explanation of how buyers actually determine these numbers, see our guide on what drives business valuation multiples when selling a business

Reduce risk and valuation follows.

These are typical Australian lower middle market observations, not guarantees.

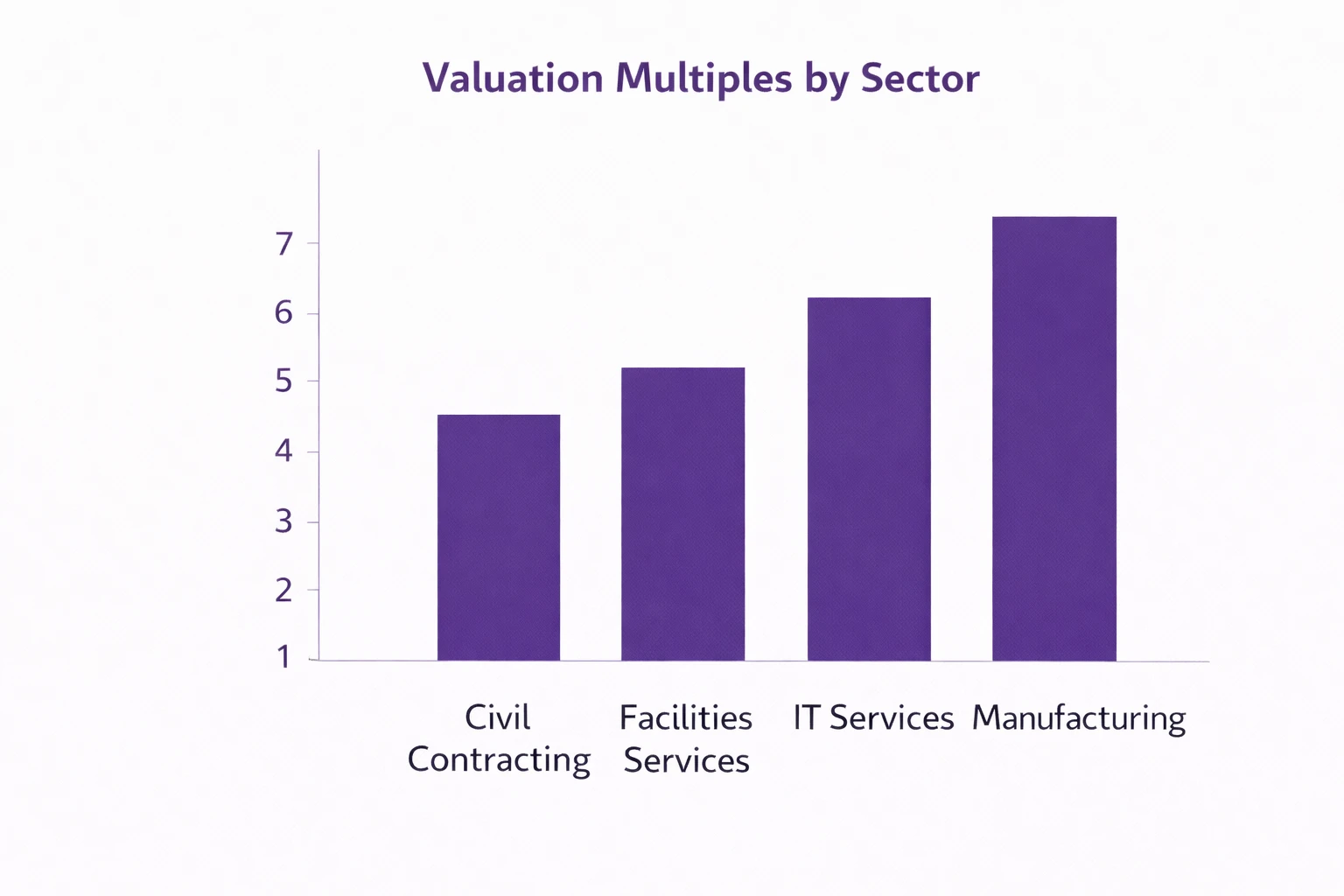

Civil Engineering Contractor

Revenue: $15M – $70M

EBITDA: $1M – $6M

Margin: 8% – 15%

Typical multiples

$1M EBITDA → 3.5x – 4.5x

$3M EBITDA → 4.5x – 5.2x

$6M EBITDA → 5.0x – 5.8x

Key risk drivers

• Project concentration

• Tender exposure

• Estimator reliance

• Bonding capacity

In project businesses, predictability commands premium pricing.

Commercial Facilities Services

Revenue: $10M – $50M

EBITDA: $1.5M – $5M

Margin: 12% – 20%

Typical multiples

$1.5M EBITDA → 4.0x – 4.8x

$4M EBITDA → 5.0x – 6.0x

Drivers

• Recurring contracts

• Supervisor structure

• Labour cost control

• Client diversification

Labour-heavy businesses trade on structure, not optimism.

IT Managed Services Provider

Revenue: $8M – $35M

EBITDA: $1M – $6M

Margin: 18% – 30%

Typical multiples

$1M EBITDA → 4.5x – 5.5x

$5M EBITDA → 6.0x – 7.0x

Drivers

• Recurring contracts

• Low churn

• Automation

• Cyber risk management

Recurring revenue compresses buyer anxiety.

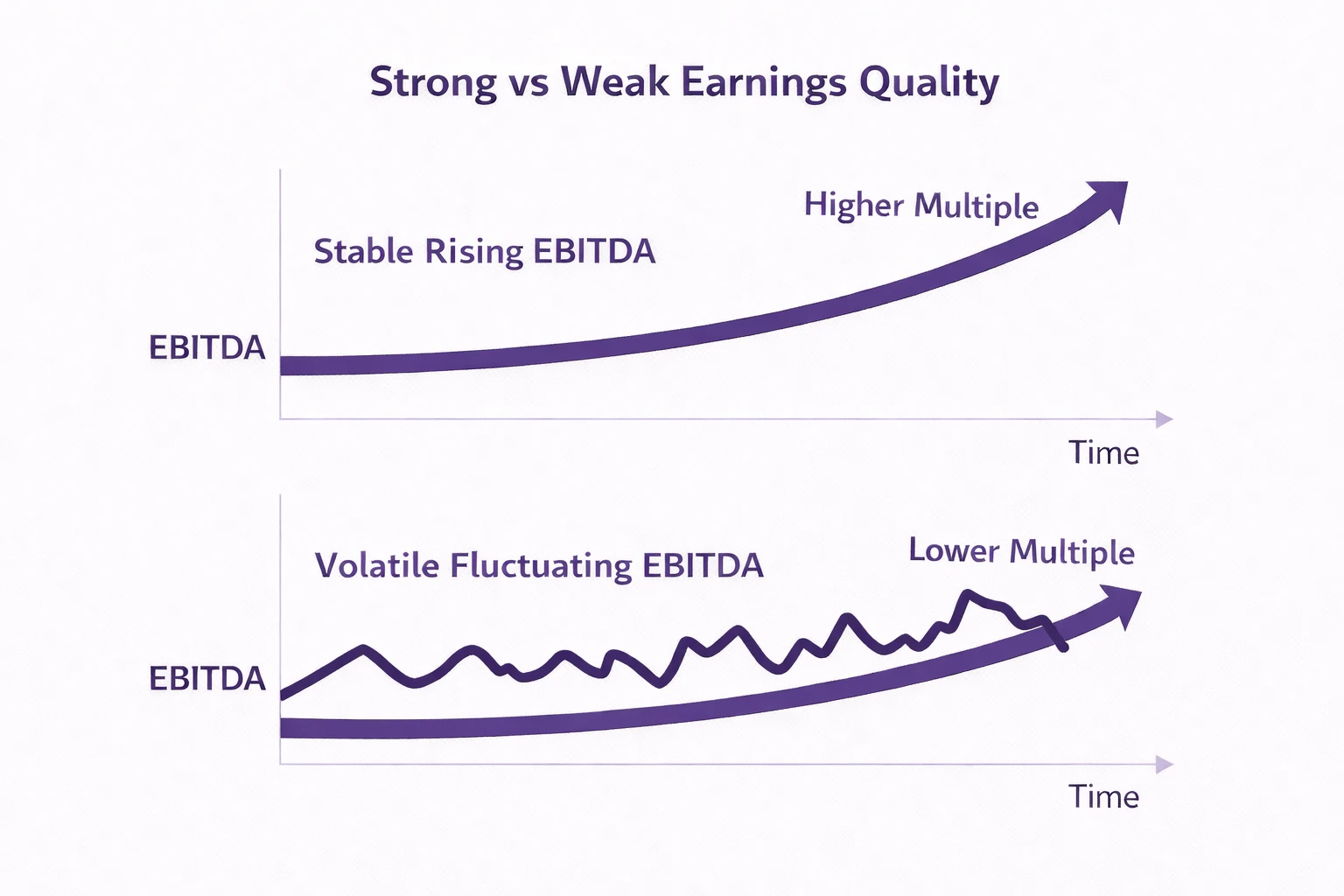

Not all EBITDA is equal.

Buyers evaluate:

• Recurring vs project revenue

• Validity of add-backs

• Working capital stability

• Historical earnings volatility

Example

Engineering firm.

EBITDA: $2.8M

If earnings fluctuate 25% annually

Multiple may compress to 4.0x

If earnings stabilise

Multiple may rise to 5.0x

That 1.0x multiple increase equals $2.8M in enterprise value.

Clean earnings create clean negotiations.

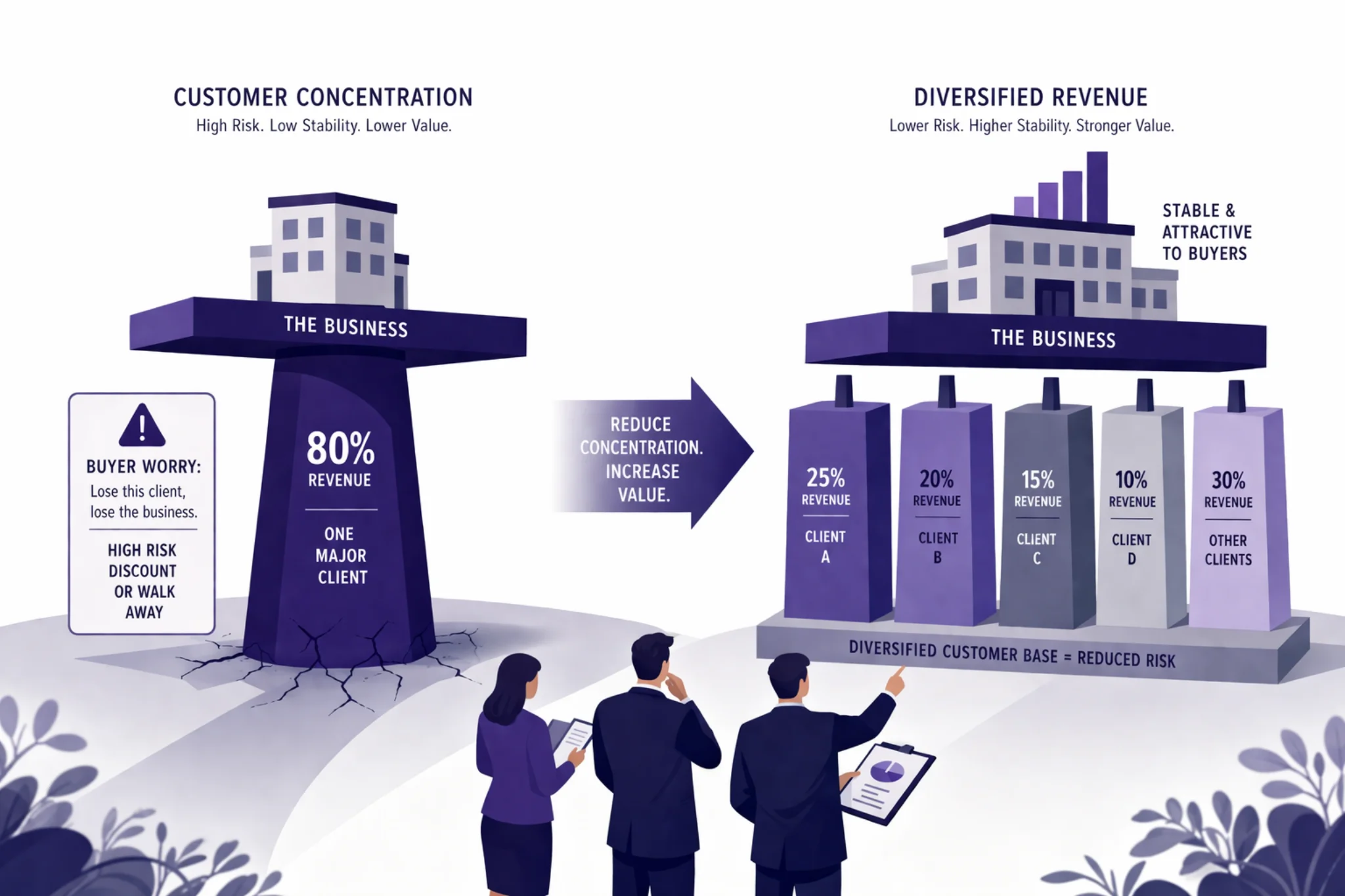

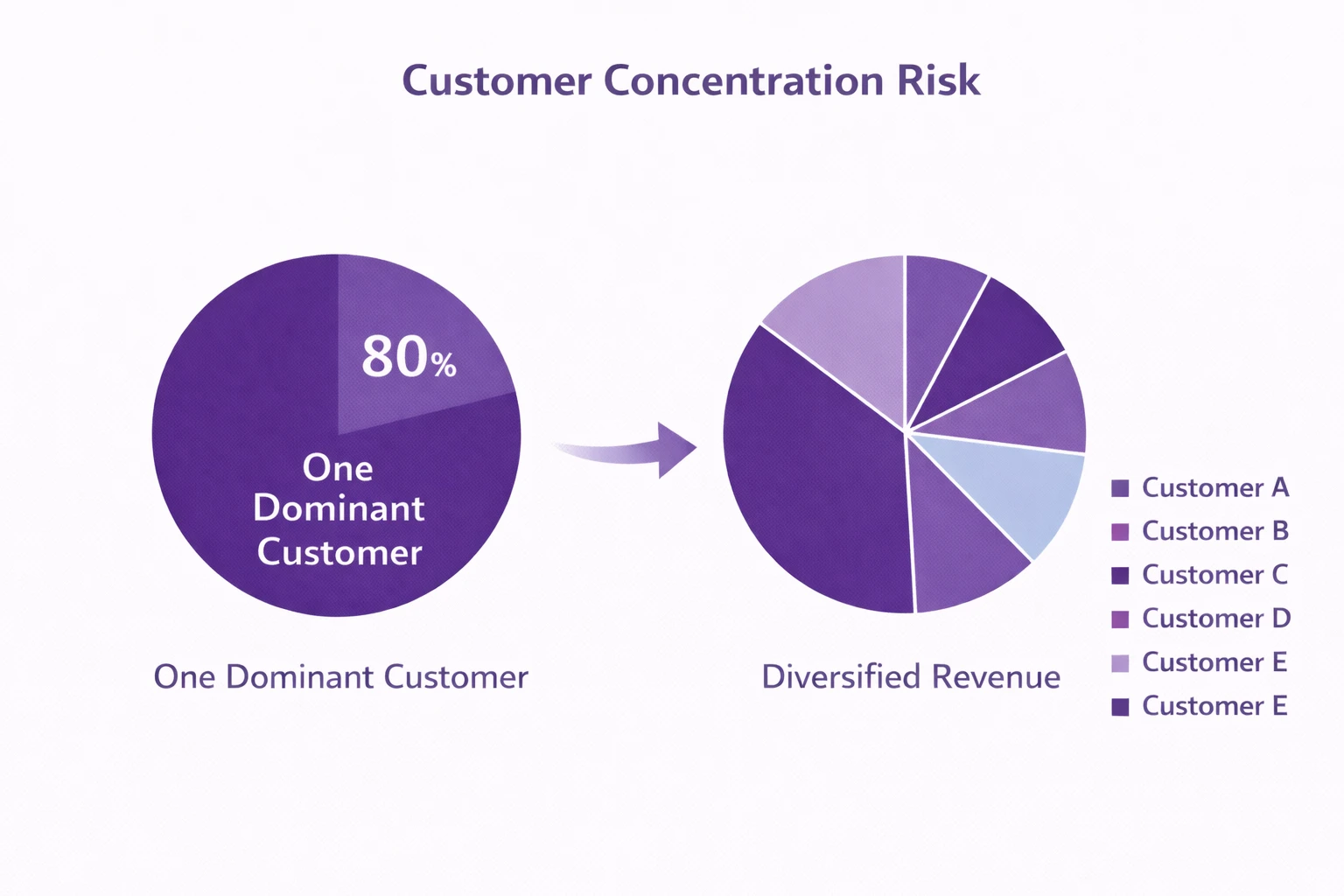

Customer concentration is one of the most common valuation discounts.

If a single client represents 40% or more of revenue, buyers price the risk of losing that customer.

Example

Manufacturing firm

EBITDA: $3.5M

Largest client: 42% of revenue

Multiple: 4.2x

After diversification to no client above 20%

Multiple increases to 5.0x

Enterprise value increases by $2.8M

Diversification materially improves valuation leverage.

Concentration creates leverage for buyers.

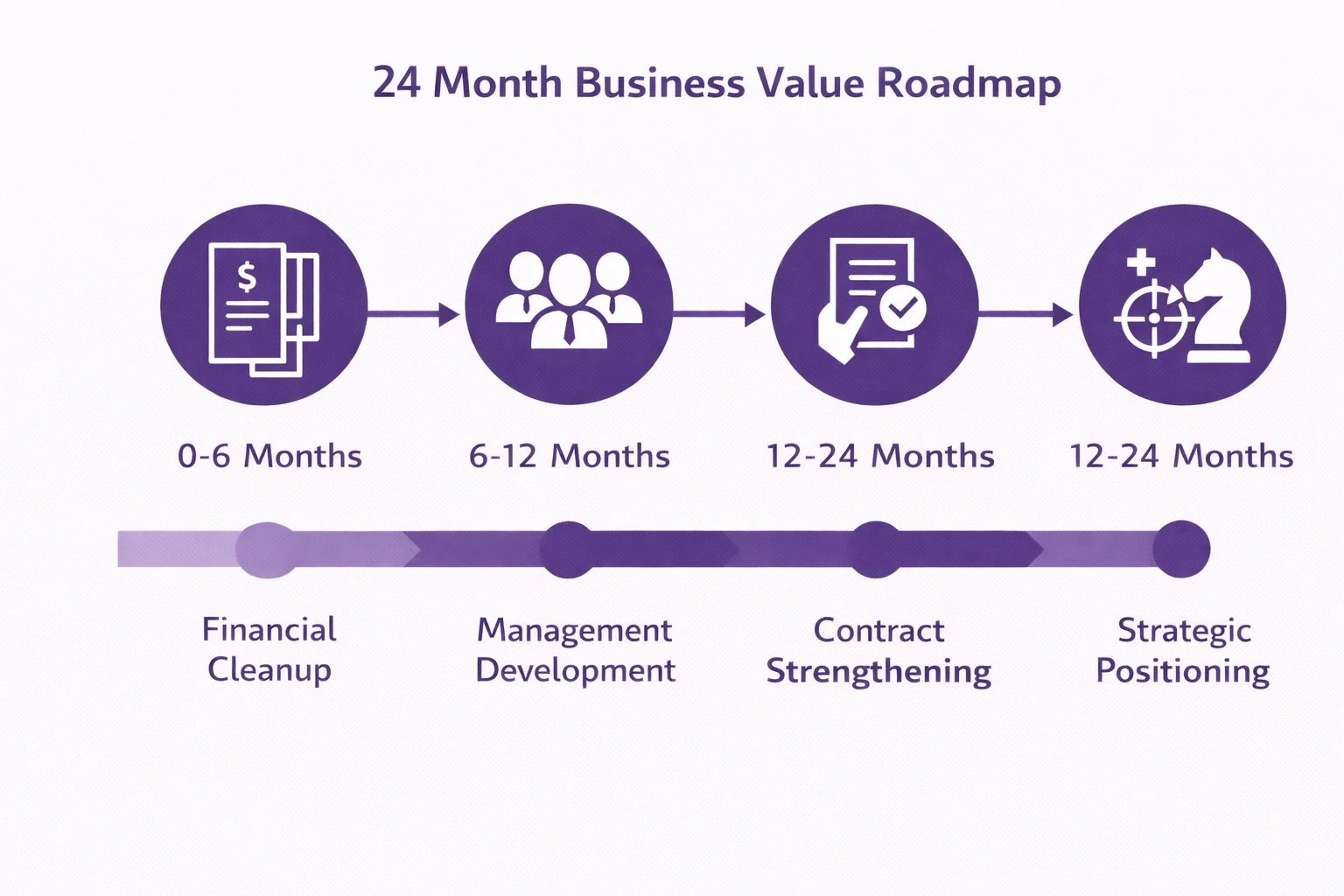

Months 0–6

• Clean financial statements

• Validate add-backs

• Improve reporting discipline

• Identify concentration risks

Months 6–12

• Diversify revenue

• Formalise management roles

• Strengthen recurring contracts

• Improve margin controls

Months 12–24

• Expand management independence

• Improve pipeline visibility

• Strengthen systems and reporting

• Position strategically for buyer interest

Preparation compounds over time.

If you want to understand where value improvements sit in the overall process, see our guide on How to Actually Sell Your Business.

Value improvement is a structured process, not a last-minute fix.

• Overstated add-backs

• Ignoring customer concentration

• Weak reporting discipline

• Owner centralisation

• Revenue chasing without margin control

• Rushing to market

Preparation determines negotiation leverage.

Preparation determines leverage.

How much can business value increase before selling?

Reducing risk can shift multiples by 0.5x–1.0x or more.

On $3M EBITDA, that can equal $1.5M–$3M in additional enterprise value.

Is increasing EBITDA the only way to increase value?

No. Often risk reduction increases multiples more than short-term earnings growth.

Can value increase in 3-6 months?

Yes, although structural improvements often require 18–36 months to fully impact valuation.

Do multiples vary by industry?

Yes. Businesses with recurring revenue and scalable models typically attract higher multiples than capital-intensive or project-based companies.

Is valuation the same as sale price?

No. Final sale price can also depend on buyer competition, deal structure and negotiation dynamics.

For Australian businesses turning over $5M–$20M with $1M–$6M EBITDA, value is not random.

It reflects:

• Risk profile

• Earnings quality

• Revenue durability

• Scale

• Transferability

• Strategic positioning

Multiples move when risk compresses.

Risk compresses when structure improves.

If you strengthen these fundamentals 12–36 months before selling, you influence both valuation and negotiation leverage.

Enterprise value reflects preparation.