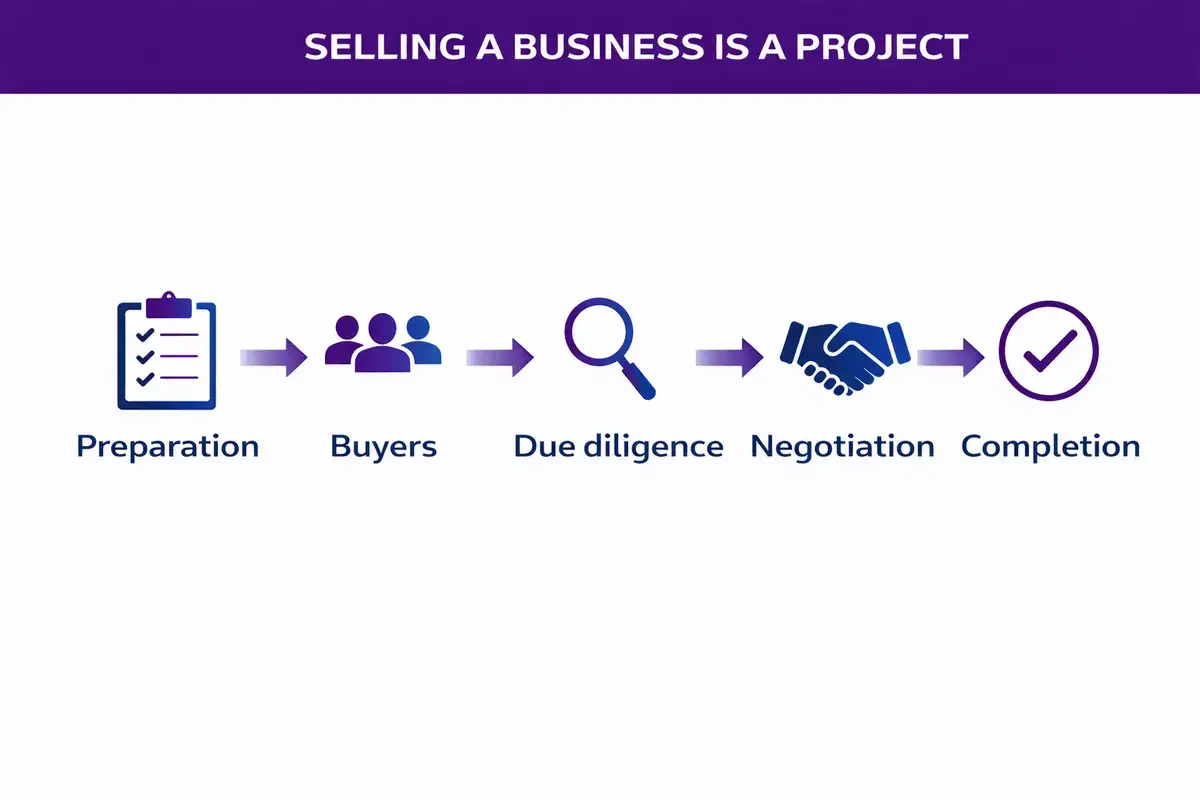

Selling a business is rarely as simple as finding a buyer and agreeing on a price.

This guide walks through the full business sale process, from the first decision to the final handover so you can move forward with clarity.

So you’re wondering how to actually sell your business.

These questions usually come up long before anyone is ready to talk about price or process.

Before going any further, it’s worth stepping back and understanding why you’re considering a sale and whether selling now is the right move for you.

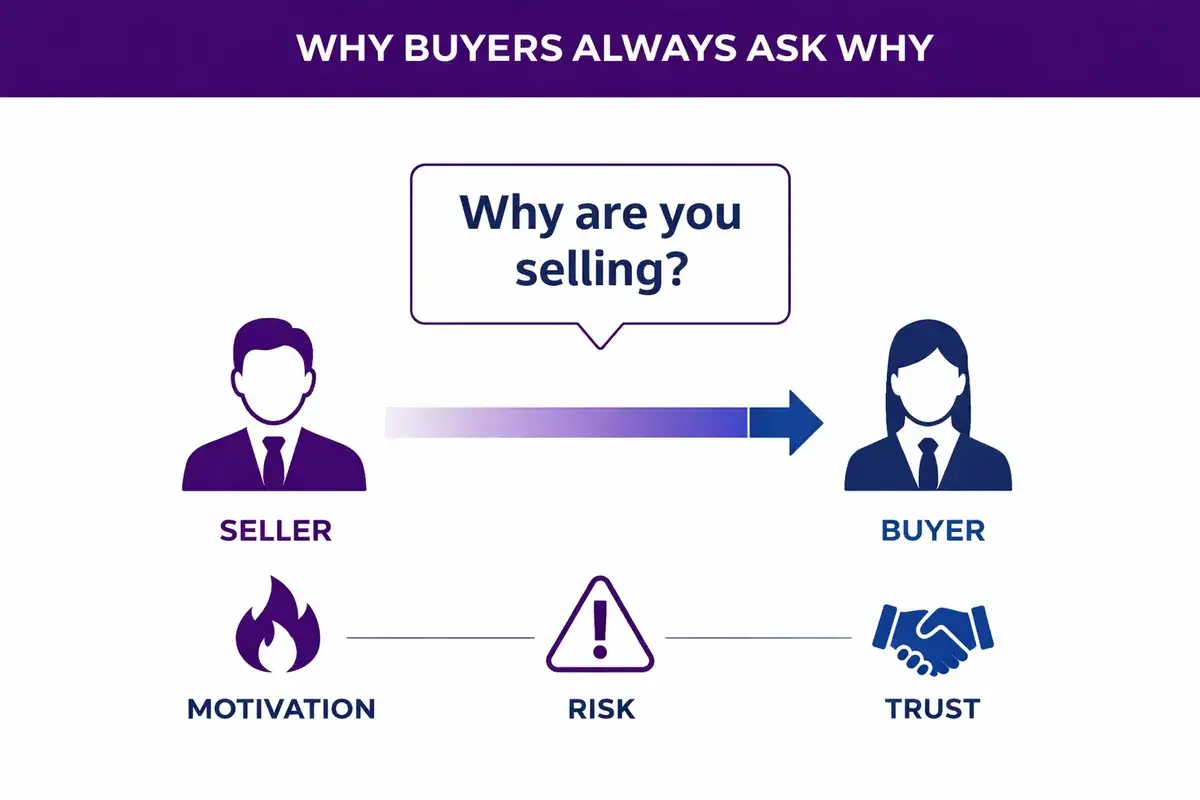

Similar to selling a car, buyers always ask one thing first. Why are you selling? Having a clear and honest answer, builds trust early and sets the foundation for the entire deal.

Feeling frustrated or stuck does not always mean selling is the right answer.

In many cases improving structure or getting clarity first can materially change the outcome.

Selling a business is rarely just about price. It’s about timing, readiness and making a decision you won’t regret later.

Most people think selling a business starts when buyers show up.

In reality the outcome is usually decided much earlier than that.

This stage is about getting ready.

Not perfection. Just clarity.

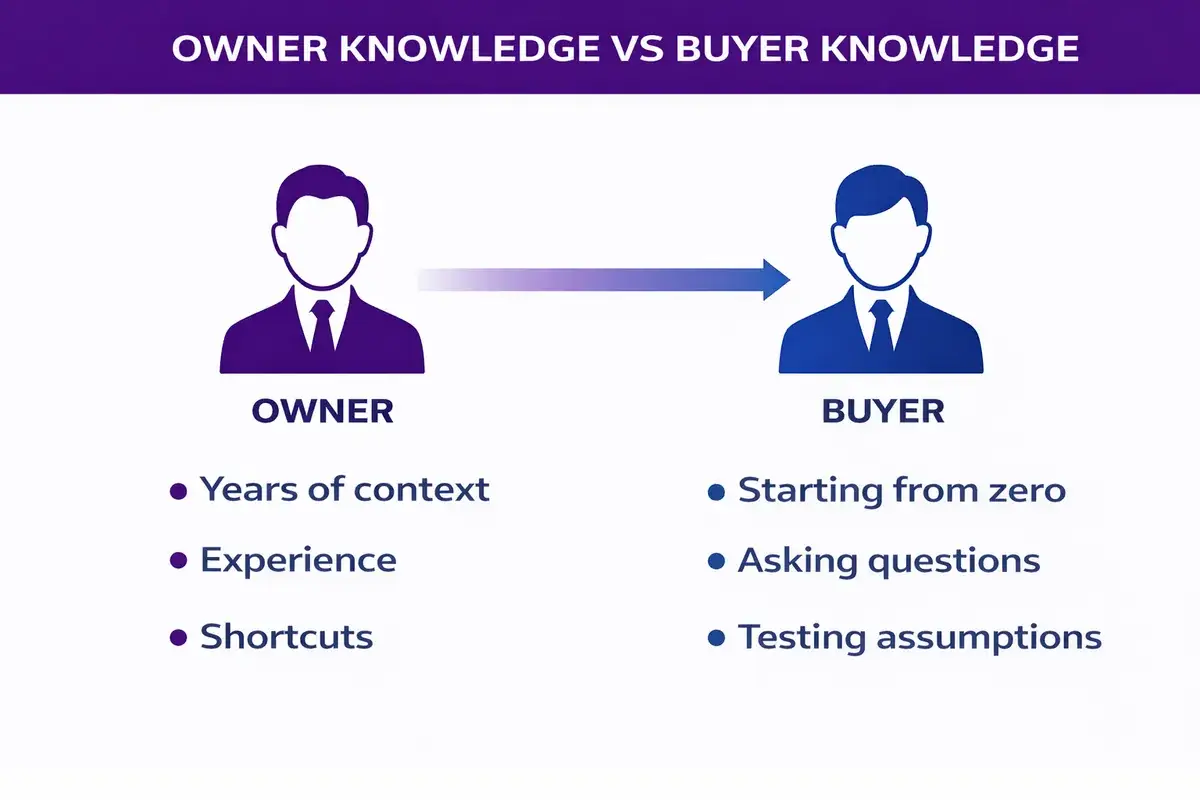

You’ve spent years getting to know your business.

What feels obvious to you is often brand new to them.

They need things broken down and clearly explained.

Assumptions create confusion. Clarity builds confidence.

Preparing for a sale is less about telling your story and more about breaking the business down so someone else can understand and take it over.

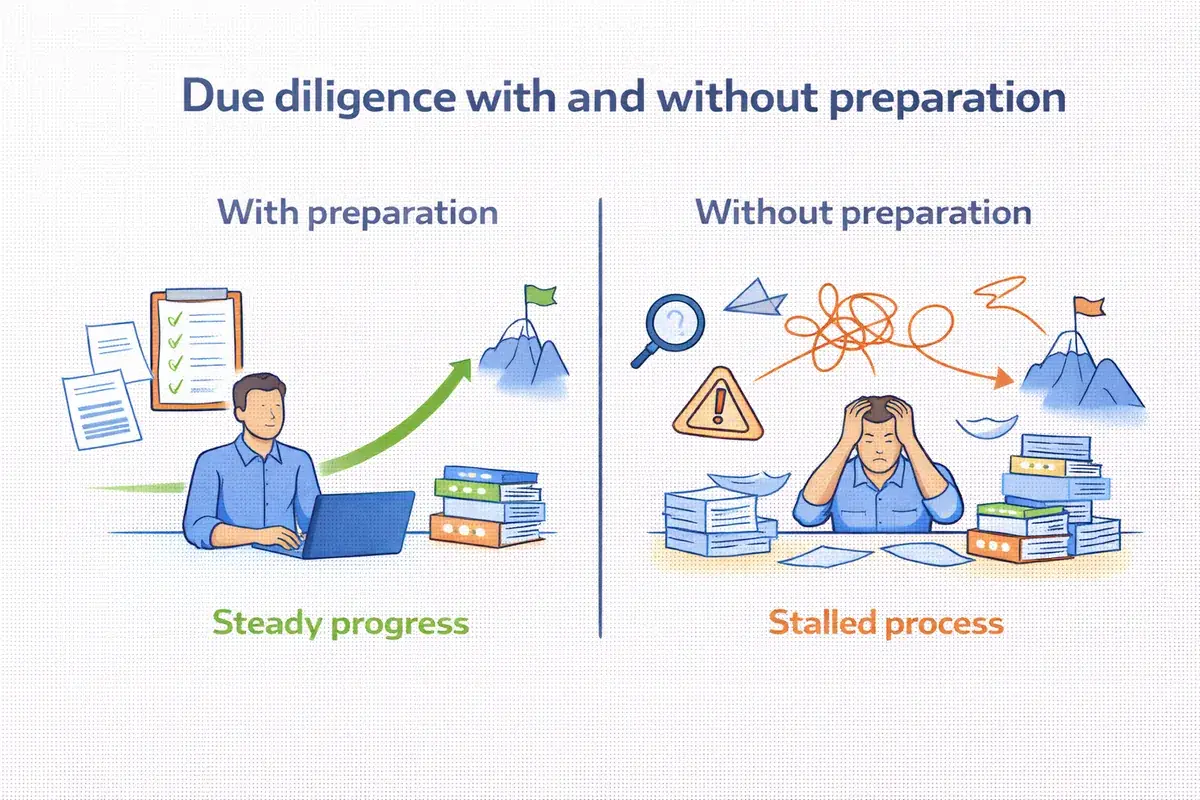

Preparation doesn’t guarantee a sale.

But poor preparation almost guarantees problems.

The better this stage is handled the smoother everything that follows tends to be.

Read up on the 11 key things to prepare before selling your business

When people start thinking about selling, one of the first questions is usually a simple one.

Getting clear on this early avoids confusion later.

But here’s the real question:

Which of these actually matter to your buyer?

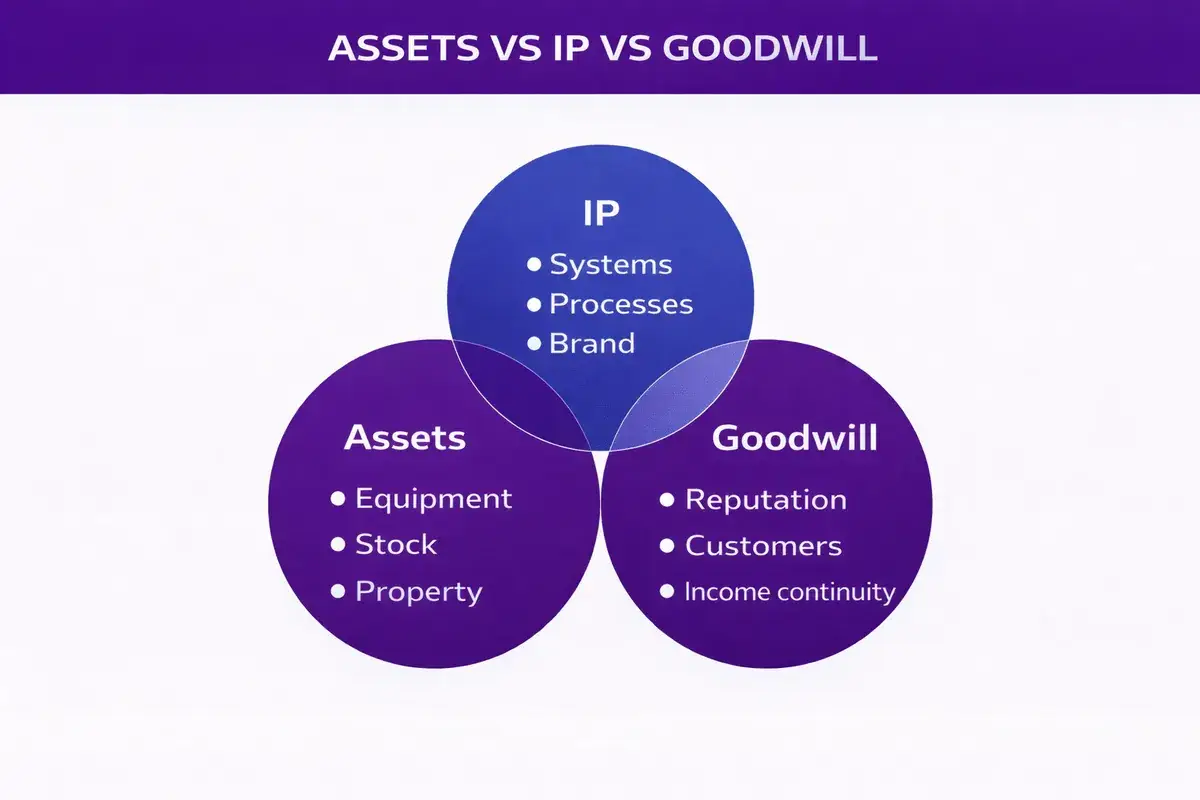

What’s included can change the value, the type of buyer you attract, and how the deal is structured.

These are terms you’ll hear a lot during a sale.

They’re also two of the least clearly explained.

Ask yourself:

A useful way to think about it:

If the doors opened tomorrow under new ownership, what would allow the business to keep working without you?

These are questions almost every owner asks at some point:

If you’re asking these, you’re not behind.

You’re just at the stage where clarity matters.

Most owners are unclear on the difference between an asset sale and a share sale at this stage. If you want a plain English breakdown, read our guide on asset sale vs share sale explained

Selling a business doesn’t mean pressing pause.

So how do you:

This balancing act is normal, and it’s one of the reasons preparation matters so much.

Understanding what is being sold, and what actually creates value, sets the boundaries for the entire deal. The clearer this is early, the fewer surprises there are later.

This is usually the part people are most curious about.

It’s also the part with the most misinformation.

If you want a detailed breakdown of how valuation actually works, including SDE, EBITDA, buyer perception and why price and valuation are not the same thing, read our guide on how to value your business and what it’s really worth

You’ve probably heard stories.

Someone sold for “X times profit”.

Another business went for a number that sounds huge.

So what’s actually true?

Two businesses can look similar on the surface and sell for very different outcomes.

Why?

Because value isn’t just a formula.

Ask yourself:

Those answers matter more than any headline multiple.

This catches a lot of owners out.

Unless a business is publicly traded, you almost never know:

So when someone says they sold for a certain amount, it doesn’t tell you much on its own.

Without context, the number means very little.

What someone says they sold for is rarely the full story. Price without terms is not a valuation.

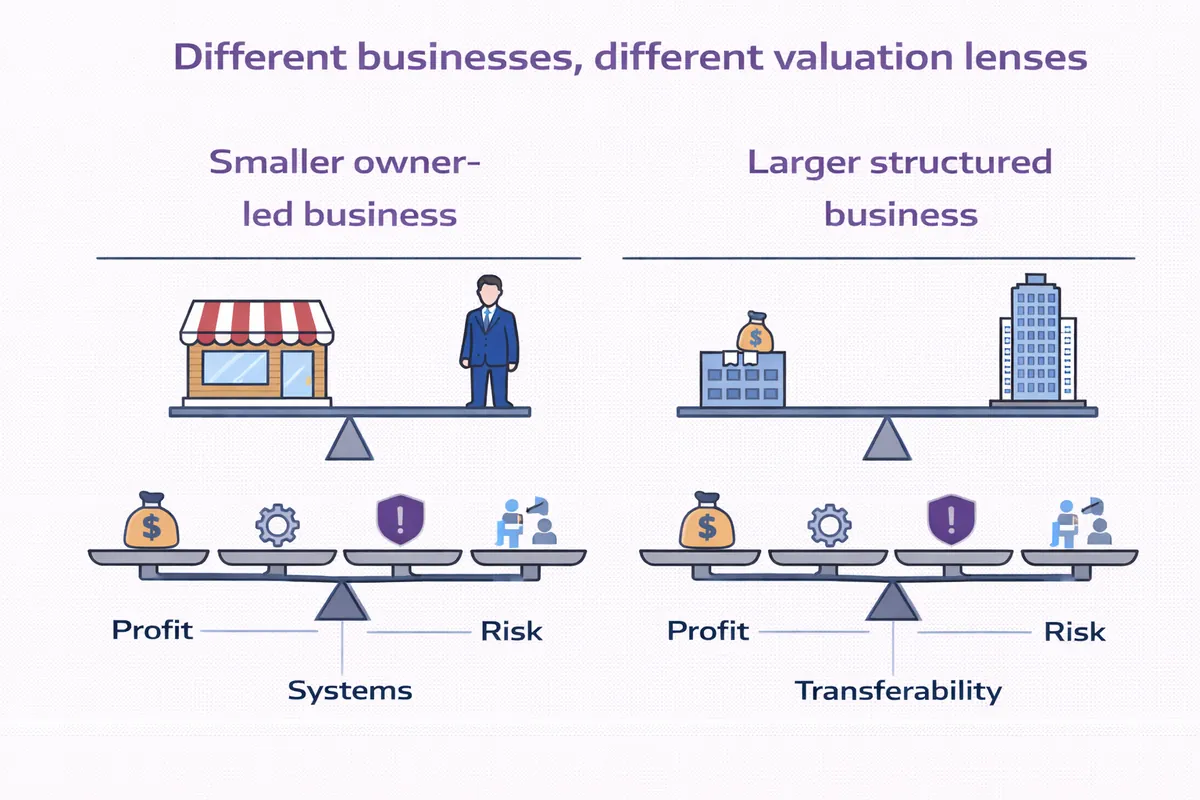

Smaller owner-operated businesses are often valued differently to larger, systemised ones.

Valuation methods can change based on:

This is why two valuations can exist for the same business, and both can be reasonable.

A competitor may value your business very differently to:

Each buyer sees;

That’s why the same business can attract very different offers.

Structure matters more than most owners realise

It’s not just what the business does.

It’s how it’s put together.

Buyers look closely at:

– How revenue is generated?

– How dependent the business is on you?

– How repeatable and transferable it is?

– How easy it would be to step in and operate?

Valuation isn’t about guessing a number or comparing stories. It’s about understanding how buyers see risk, opportunity, and transferability. Once you understand that, the numbers start to make sense.

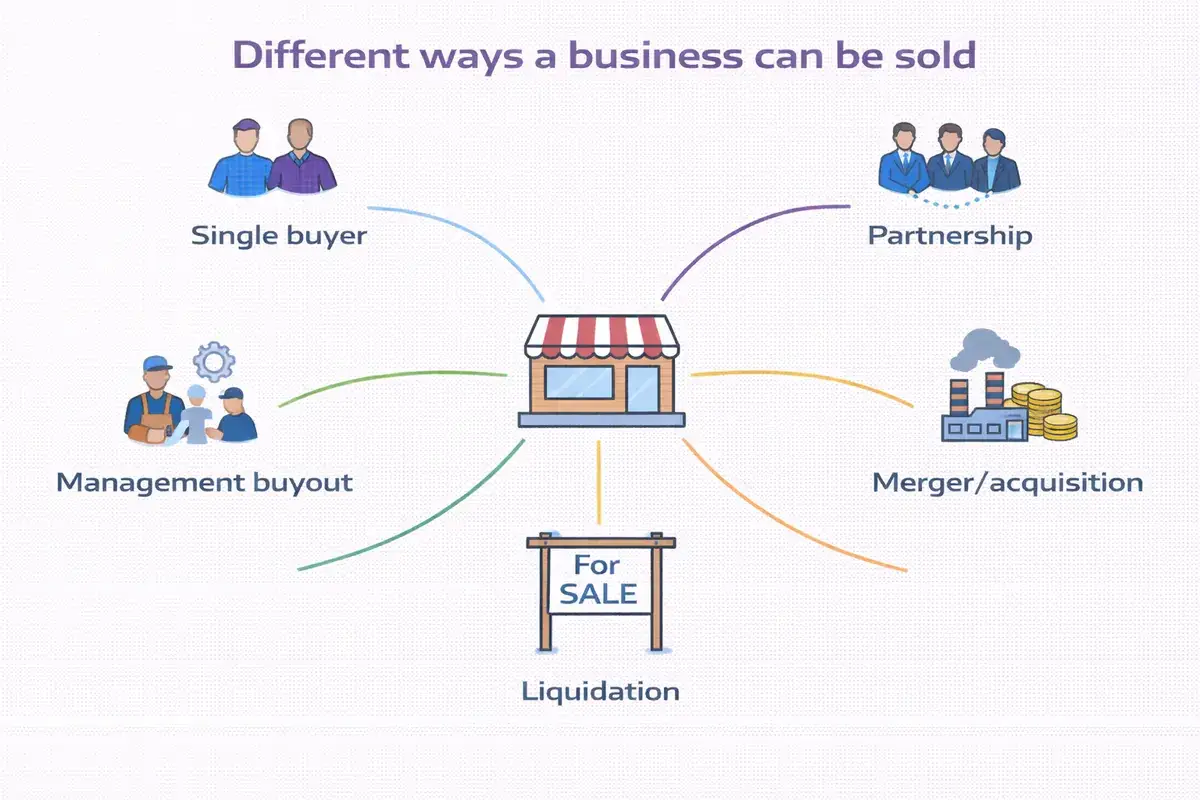

Most owners think there’s only one way to sell a business.

Put it on the market, find a buyer, agree on a price, move on.

In reality, there are a few different ways a sale can happen, and the path you take can change:

Not all buyers want the same thing.

And not all sellers want the same outcome.

That’s why sale structures vary.

If you are trying to understand what those structures mean for your life after settlement read how long do I have to stay after selling my business.

None of these are right or wrong.

They just come with different trade-offs.

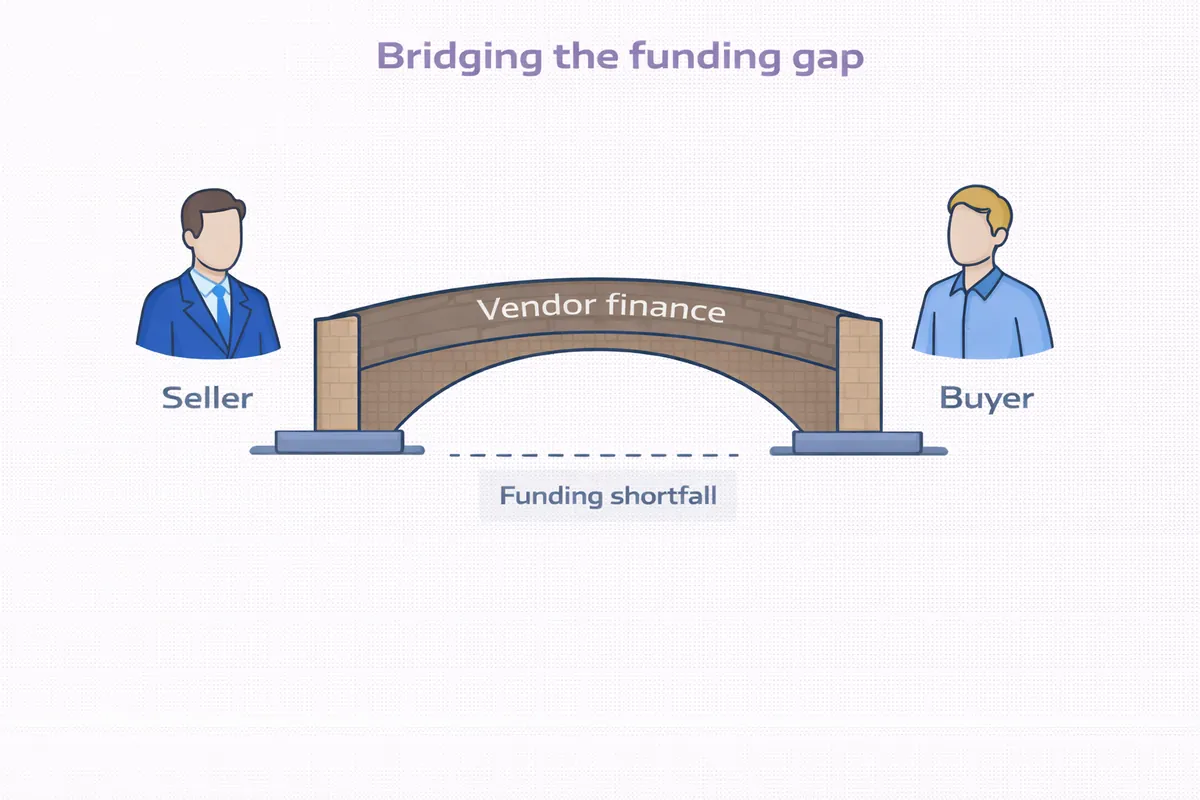

Sometimes the right buyer for the business doesn’t have all the funds upfront.

In these cases, the seller may agree to finance part of the deal.

This means you receive some of the sale price over time rather than all at once.

It’s not about discounting the business.

It’s about bridging a funding gap to get a good deal across the line.

Vendor finance is often used when:

Like any structure, it increases flexibility but also changes the risk profile.

It needs to be thought through carefully and documented properly.

More attention to detail now means less stress later.

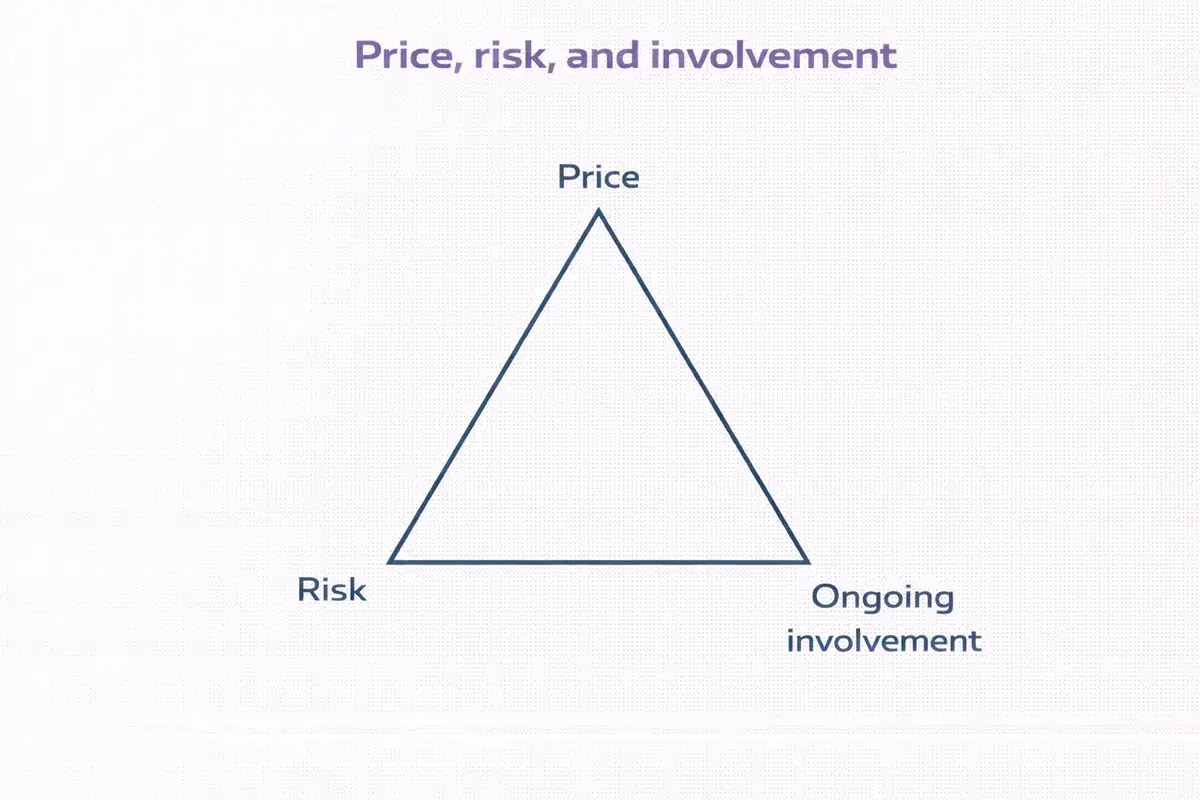

Two deals can look the same on paper and feel very different in real life.

It’s worth asking:

A higher price doesn’t always mean a better outcome.

Most deals are a balance between price, risk, and how involved you stay after the sale.

Some owners choose to:

This approach can suit owners who want flexibility or aren’t ready for a full exit yet.

A fast deal isn’t always a good deal.

Problems tend to show up when:

The way a deal is set up should make life easier, not harder.

How a business is sold matters just as much as who buys it. The structure you choose shapes the risk you carry, and what comes next for you.

Finding a buyer isn’t usually the hard part.

Finding the right buyer is.

Not everyone who shows interest should be taken seriously.

And not every buyer who sounds good early will be right in the end.

This stage is about choosing carefully, not moving fast.

If you’re unsure what types of buyers are even realistic for your business, it helps to first understand who could actually buy it and why.

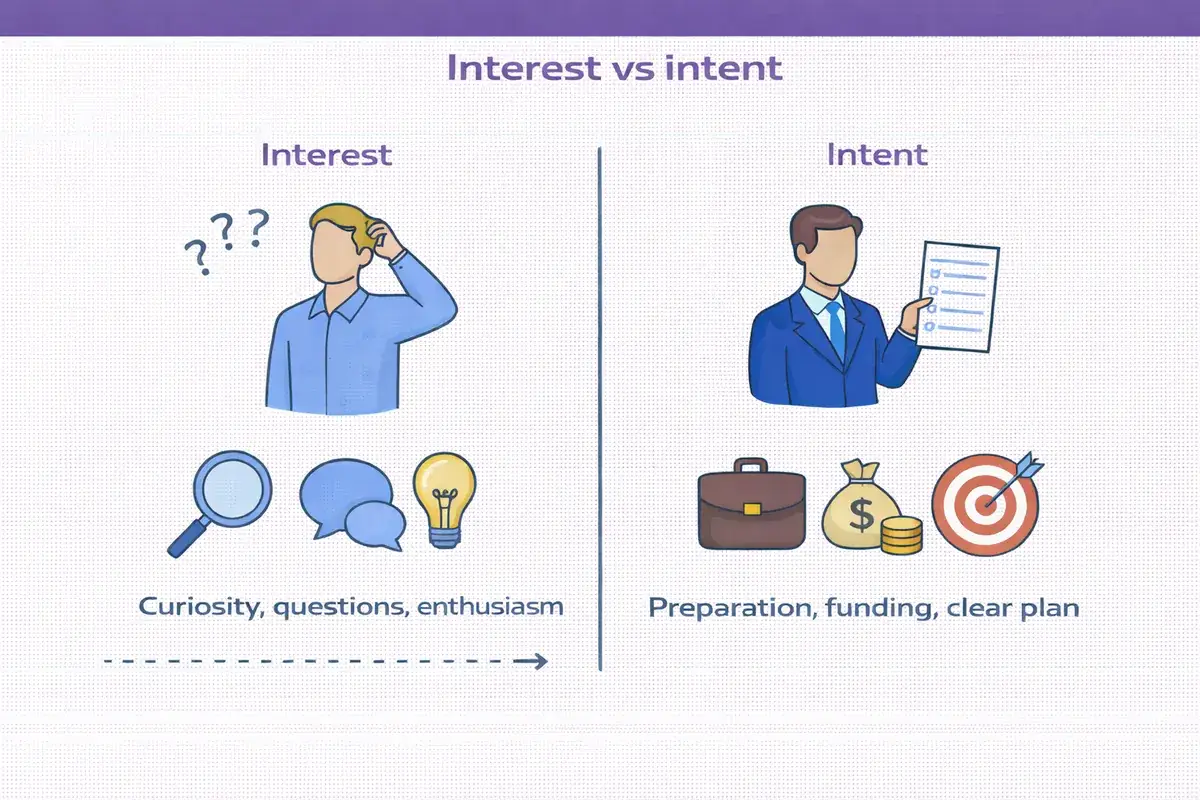

A buyer asking questions doesn’t mean they’re ready to buy.

Talking about price doesn’t mean they can complete the deal.

Before going too far, it’s worth asking:

Most problems later on can be traced back to poor filtering early.

Common mistakes include:

Time spent with the wrong buyer is time taken away from running the business.

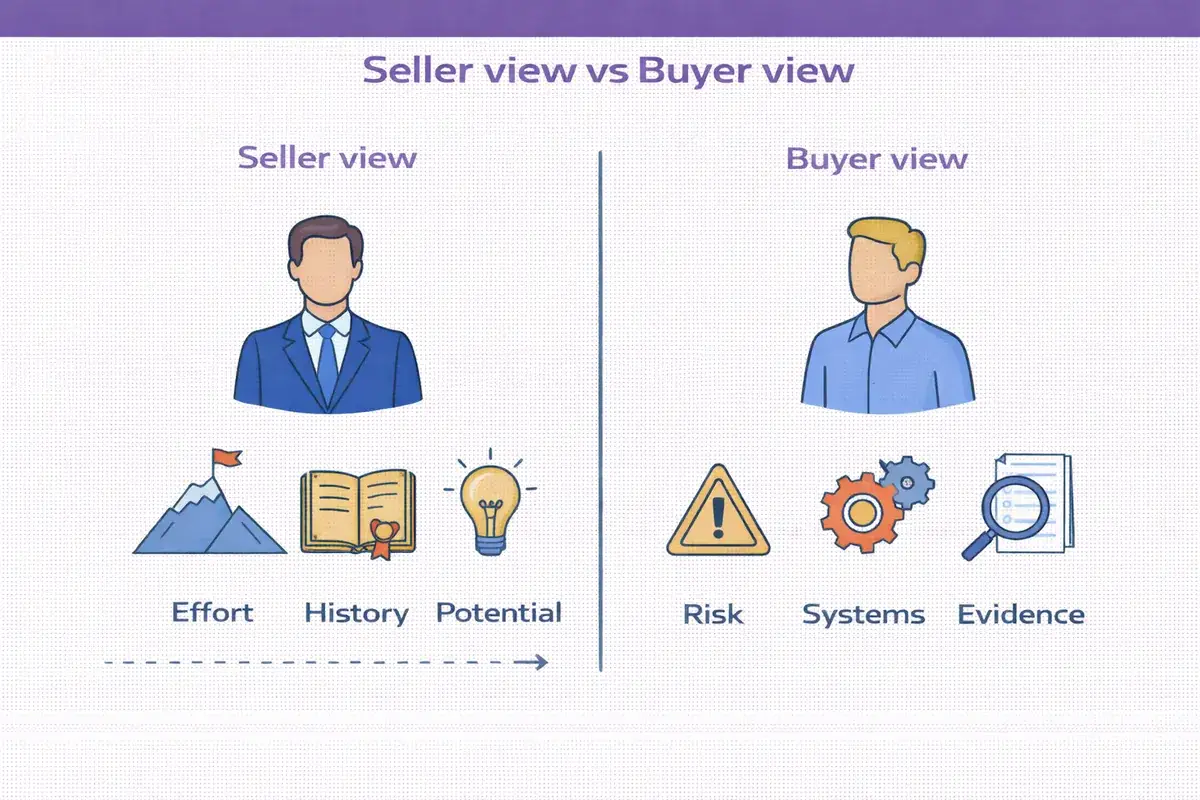

Buyers aren’t trying to be difficult. They’re trying to reduce risk.

They’re usually thinking about:

When sellers understand this, conversations become calmer and clearer.

When a buyer pushes on a detail, they’re usually testing risk, not doubting you.

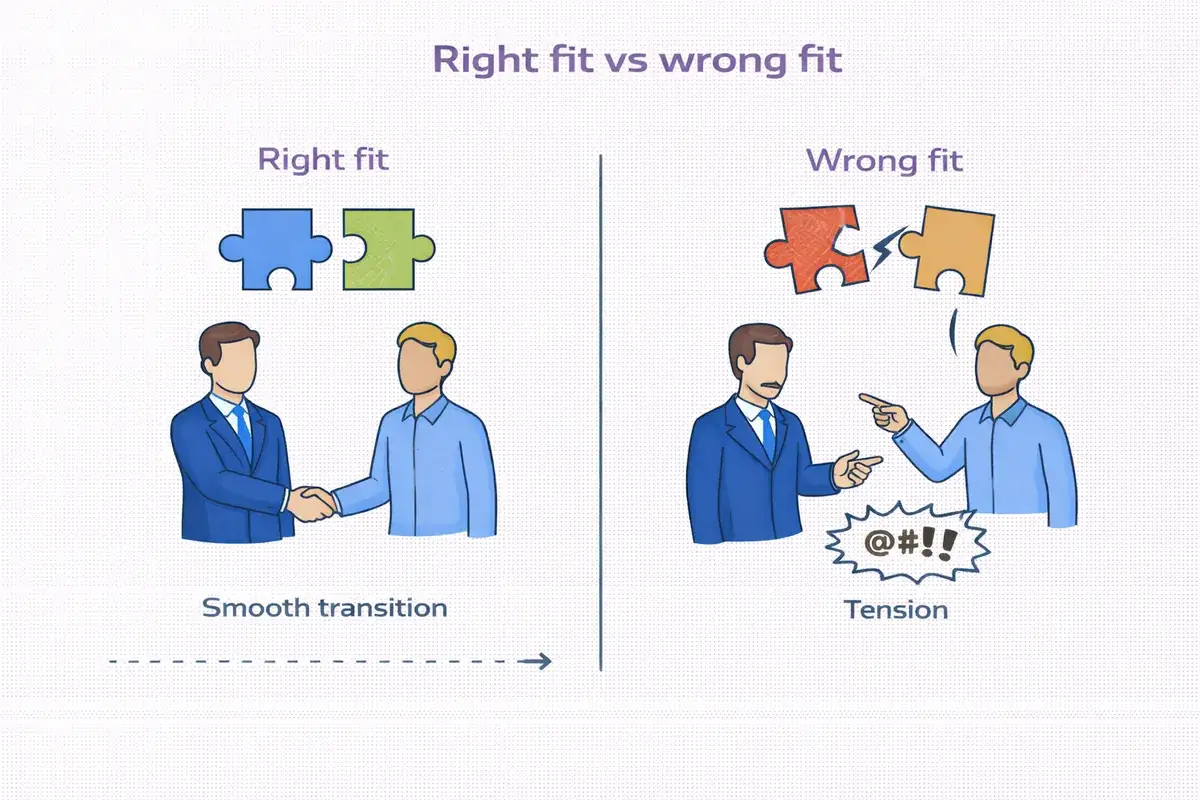

A buyer can sound enthusiastic and still be the wrong fit.

Problems often show up when:

A good fit usually feels steady, not rushed.

At this stage:

The goal isn’t to find any buyer. It’s to find the right buyer for the business, and the outcome you want. Get this right, and the next stages are far simpler.

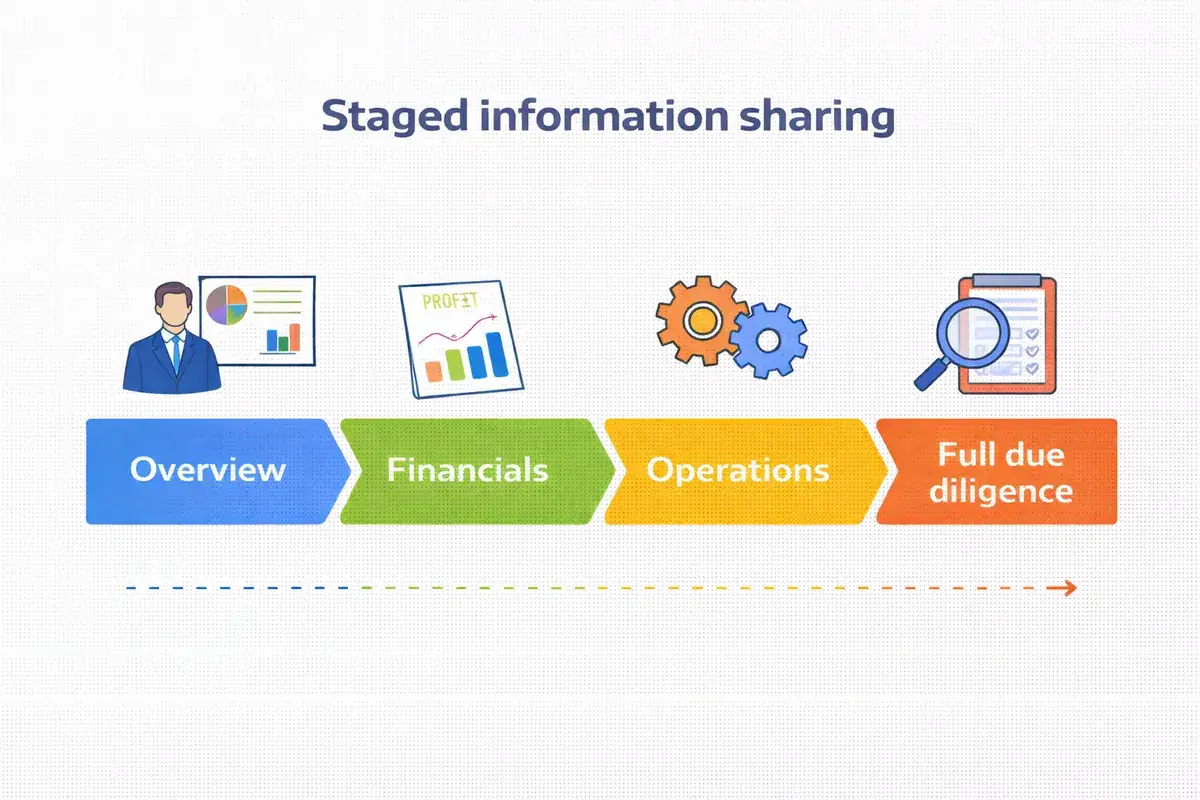

This is the stage most deals are won or lost.

Up to this point, things are mostly conversations.

Now the buyer starts checking whether what they’ve been told matches reality.

This process is usually called due diligence, but at its core it’s just verification.

Buyers are not trying to catch you out.

They’re trying to get comfortable.

They want to confirm:

The more confidence they gain here, the smoother everything else becomes.

Most problems at this stage are avoidable.

Common issues include:

None of these help a buyer feel confident.

Trying to smooth things over early almost always backfires later.

Buyers expect:

What they struggle with is:

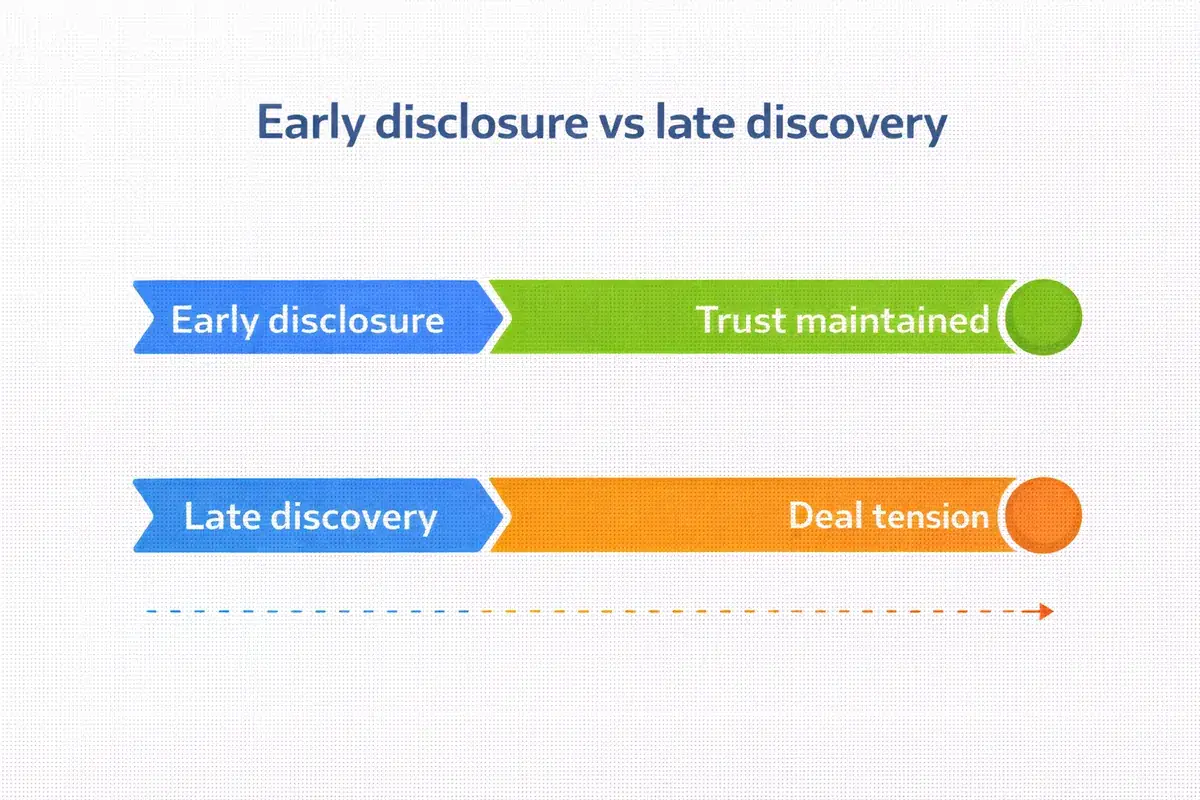

Small issues disclosed early are usually manageable. Small issues discovered late rarely are.

This stage can feel personal.

Owners may feel:

Buyers may feel:

Keeping conversations factual and calm helps prevent unnecessary friction.

Poor or uncoordinated advice can complicate this stage quickly.

Problems often arise when:

Due diligence isn’t about perfection. It’s about alignment between what’s been said and what can be shown. The closer those two are, the easier this stage becomes.

This is the point where things stop being theoretical.

You’re no longer just talking about the business.

You’re talking about the deal.

If this stage feels a little uncomfortable, that’s normal.

It usually means you’re close.

There is no deal where only one side sets the rules.

That doesn’t mean the deal is weak.

It means both sides are trying to make it work.

And that’s usually a good sign.

Two offers can look the same at first glance and feel very different once you slow down.

This is where many owners pause and think,

“Hang on… what am I actually agreeing to here?”

That’s a healthy reaction.

It’s worth asking:

A higher number on paper doesn’t always mean a better outcome in real life.

In many sales, not everything is guaranteed from day one.

That might include:

This doesn’t mean the buyer doesn’t trust the business.

It usually means they’re trying to manage uncertainty.

If a term doesn’t feel right now, it usually won’t feel better later.

Before you commit, it helps to pause and get clear.

Ask yourself:

There’s no perfect answer.

There is a right answer for you.

This stage can feel stressful.

Details pile up.

Deadlines appear.

Emotions can sneak in.

Staying calm and respectful often leads to:

Even good buyers usually need some help early on.

That might mean:

This doesn’t mean you’re stuck.

It usually means you’re helping set the business up to succeed.

f you want to go deeper on terms, risk balance and keeping momentum, read our guide on how to negotiate a business sale with a buyer

This stage isn’t about rushing to the finish line. It’s about agreeing to terms you still feel comfortable with once the dust settles. Get this part right, and the final steps feel far less stressful.

By this stage, it’s clear the deal involves more than just you and the buyer.

There are other people involved.

And how well they work together has a big impact on how smooth this feels.

This part is about having the right support and keeping everyone aligned.

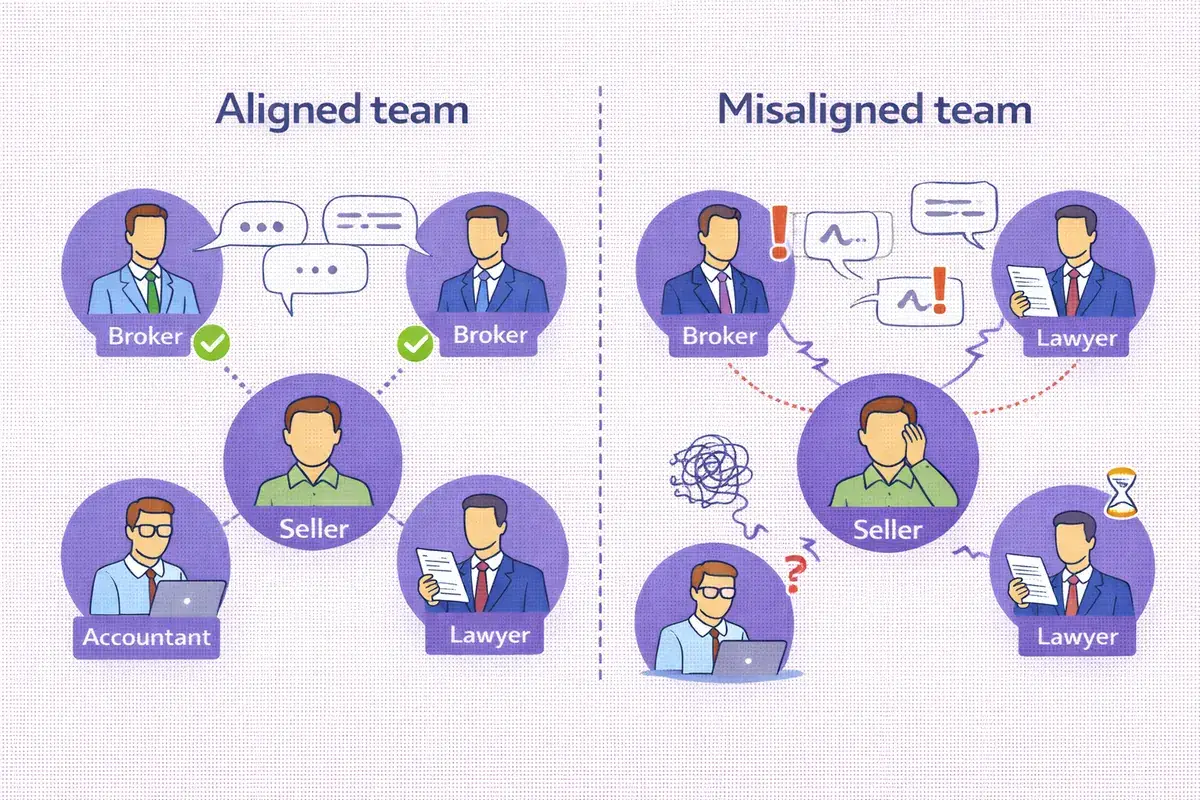

Lawyers, accountants, and brokers all play a role in a business sale.

When they’re right for the job, they help:

When they’re not, things slow down or become harder than they need to be.

This is a common issue.

A good professional in one area isn’t always right for selling a business.

Problems usually arise when:

It’s reasonable to pause and make sure everyone understands the goal.

Business brokers sit in the middle of the deal.

They often help with:

But not all brokers work the same way.

There are brokers.

And then there are good brokers.

A good broker is more than a go-between.

They tend to be:

Their job is to:

A good broker reduces confusion.

A poor one often adds to it.

Employees are one of the most sensitive parts of a sale.

Telling them too early can create uncertainty.

Telling them too late can damage trust.

Owners often ask:

There’s no perfect moment.

But there is a better order.

In many businesses, relationships are a big part of the value. Buyers will care about client stability, supplier arrangements & how relationships transfer. Careful timing and clear communication help protect these relationships.

Delays often come from:

These don’t mean the deal is failing.

They usually just mean more care is needed.

Selling a business isn’t just about choosing a buyer. It’s also about the people helping you through the process. The right team makes this stage easier and sets up a smoother handover.

This is the part most owners look forward to.

It’s also the part where expectations matter most.

The deal may be agreed, but the journey isn’t quite finished yet.

This stage is about transition, payment, and setting yourself up for what comes next.

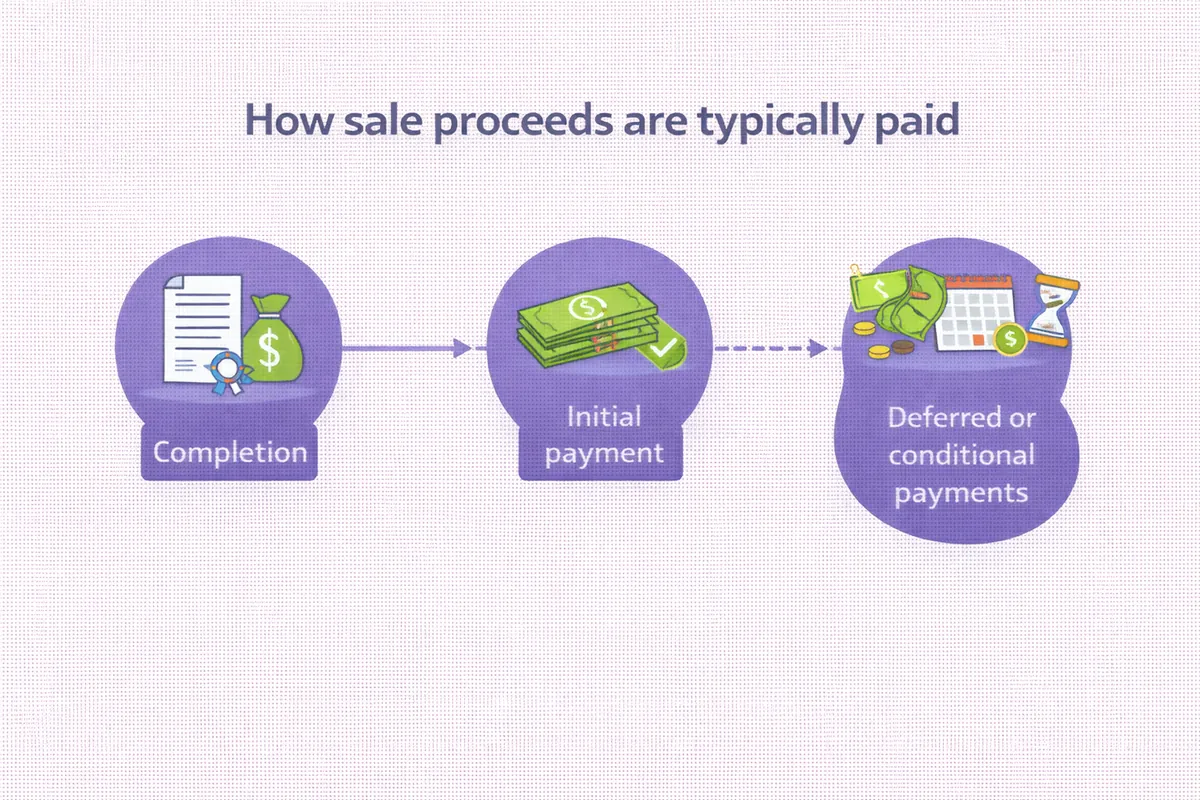

Very few deals involve everything being paid in one clean hit on day one.

Payment may include:

Understanding the timing and conditions helps avoid surprises.

Even in the best transactions, buyers usually need support early on.

That might involve:

This doesn’t mean you’re trapped.

It usually means you’re helping protect the value you’ve just sold.

Before final settlement, a few practical things are usually worked through.

These can include:

None of this is unusual.

It’s part of closing things properly.

This part is often overlooked.

After years of running a business, stepping away can feel strange.

Some owners:

There’s no right answer.

It helps to think about this before the deal completes.

Selling a business changes more than your bank balance.

It changes your routine, identity, and pace of life.

Selling a business is rarely a single moment. It’s a process that rewards preparation, patience, and clarity. Handled well, it doesn’t just end one chapter. It sets up the next one properly.