When a buyer appears, unfamiliar language tends to surface very quickly.

One of the first phrases business owners hear is asset sale vs share sale.

Often both.

Usually without much explanation.

At that point, many owners nod along without really knowing what either term means, or why it suddenly matters.

This article explains the difference in plain English, so the structure itself stops being a source of confusion.

If you are exploring the broader process, you can read our complete guide on how to actually sell your business.

Most owners encounter these terms only once a buyer is already at the table.

An asset sale is when the buyer purchases specific parts of the business.

That can include:

The legal company itself is not sold.

The seller keeps the company, along with anything not transferred.

In an asset sale, the buyer chooses what they take. The company stays behind

From the buyer’s perspective, this limits what they inherit.

From the seller’s perspective, it means selling components rather than ownership.

In Australia, this structure usually means tax is triggered across the assets sold, often within the company rather than personally.

The outcome depends on what is sold and where the value sits.

A share sale works differently.

Here, the buyer purchases the shares in the company that owns the business.

Nothing is broken apart.

The following move together under new ownership

Contracts

Employees

Liabilities

History

For many owners, this feels simpler.

One transaction

One exit

From a tax perspective in Australia, sellers are usually taxed at the shareholder level rather than at the asset level.

This is why many owners initially assume a share sale is always preferable.

That assumption rarely considers the buyer’s position.

Ownership changes but everything underneath stays in place.

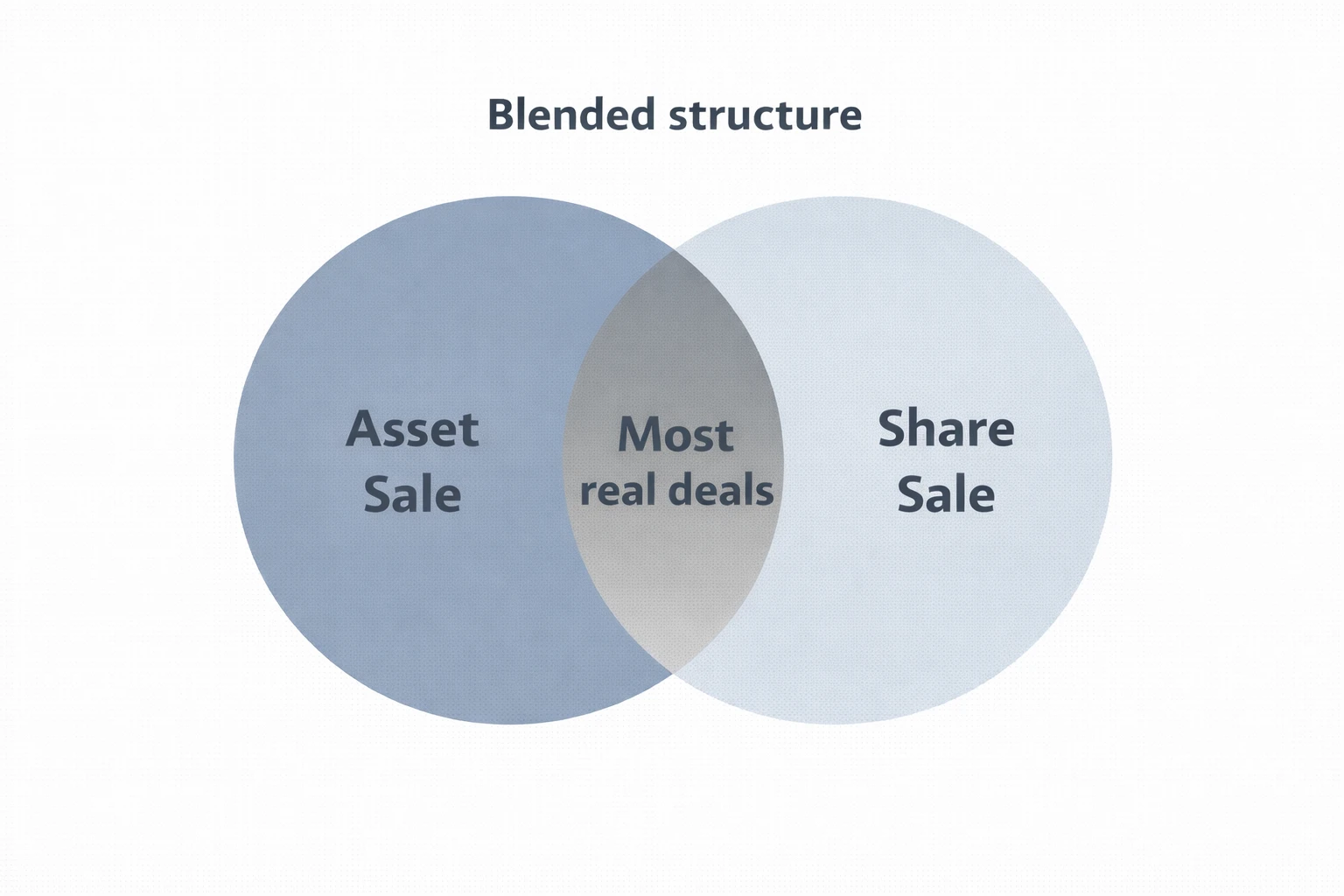

In practice, most transactions sit somewhere in between.

A deal may be described as a share sale but

Exclude certain assets

Exclude specific liabilities

Or it may be an asset sale that

Leaves licences behind

Leaves contracts behind

Leaves historical obligations behind

The labels describe the framework not every moving part.

This is where balance matters.

Buyers and sellers approach structure from different angles and the final outcome is often negotiated rather than textbook.

Real deals are usually blended even if they’re described as one or the other.

Structure affects more than legal form.

It shapes

How tax is triggered

What risks move to the buyer

What the seller retains

How clean the exit feels in practice

These differences can materially change outcomes even when the price stays the same.

Often this only becomes clear once both sides understand what is actually being transferred.

The price can stay the same while the outcome changes materially.

Think of a construction business.

Most of its value sits in

Machinery

Vehicles

Contracts

People

Buyers often focus on specific assets they need to operate.

In this context, asset-focused structures are common.

Even then, licences or contracts may remain with the company creating a blended outcome rather than a clean split.

When value sits in equipment assets naturally become the focus.

Now consider an IT or software services business.

There may be few physical assets.

Most value sits in

Intellectual property

Contracts

People

Here, share sales are more common because separating assets would be impractical.

Even so, founders may retain certain IP or exclude non-core assets again creating a blended structure.

When most of the value sits within the company itself, it is the ownership that typically transfers.

Most resistance appears once tax is mentioned.

Both buyers and sellers want to minimise it.

They just approach it differently.

Asset elements can benefit buyers.

Share elements can simplify exits for sellers.

That tension is usually resolved through compromise rather than purity.

Tax is rarely the whole story but it’s where tension usually shows up.

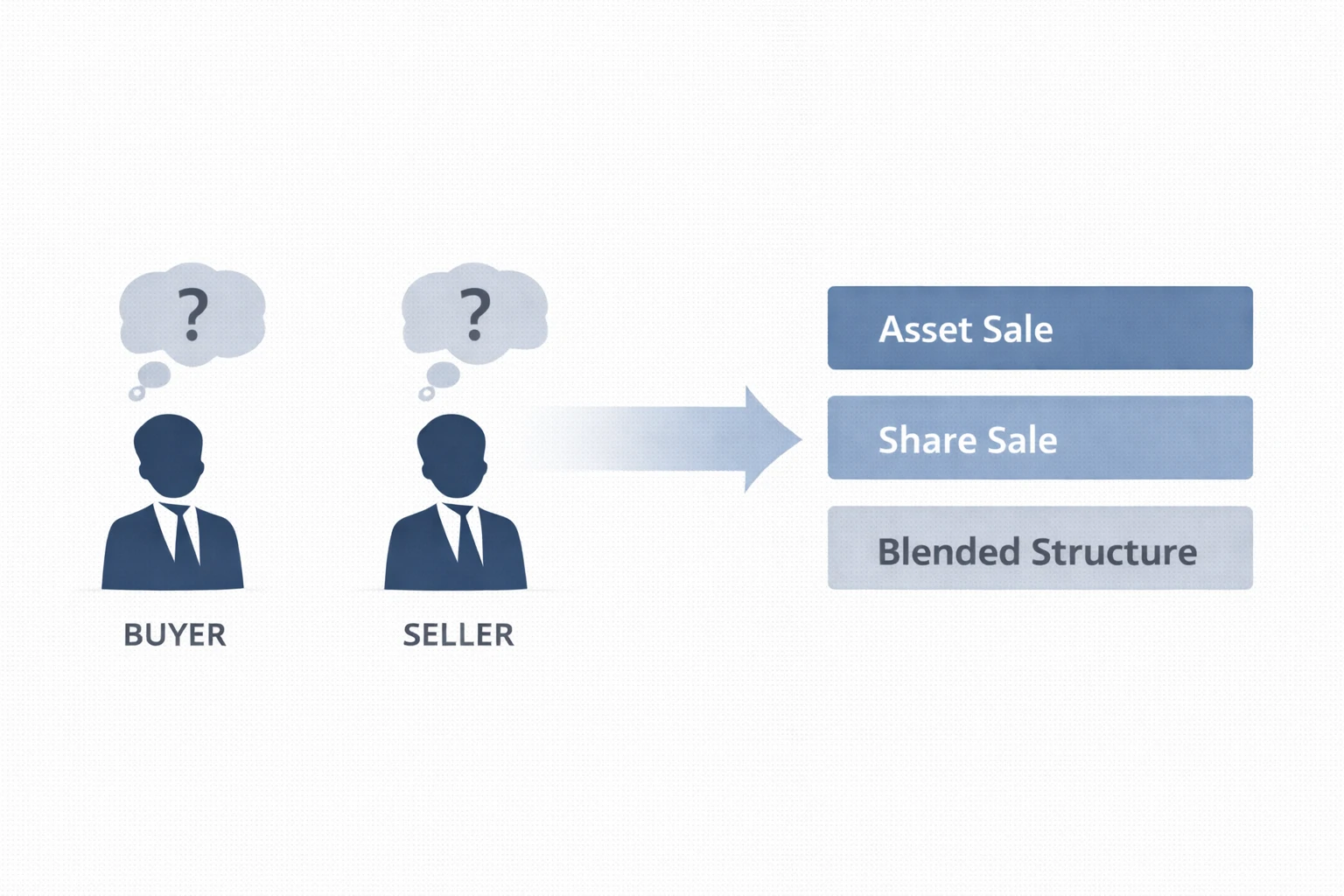

Many owners assume

One structure is always better

The seller decides unilaterally

Structure is just a legal detail

In reality, structure shapes risk, tax and outcomes. It is rarely an afterthought

Asset sale and share sale are not strategies.

They are frameworks.

And in practice, they are often combined.

Understanding the language does not dictate what should happen.

It simply allows owners to engage in the conversation without guessing.

Later in the sale process, structure influences

Tax outcomes

Risk allocation

How complete the exit feels

If you would prefer guidance on how structure fits into your specific situation, you can learn more about our business sale advisory services here.

For now, understanding the difference is enough.

Clarity comes before decisions.